The Constant

Starting at Impressions front desk in 2006 when he was 19 years old, General Manager Paul Petrowsky is a seasoned professional who owner Sarah Taylor says is responsible for much of her own success.

by Stacey Soble

The IRS may enforce penalties, interest, or even jail time if you misclassify your workers. This guide is designed to help you avoid that mess and determine who should receive a 1099 and who truly needs a W-2.

While classifying workers as independent contractors may seem more manageable, failure to classify properly can lead to serious legal trouble.

Pixabay

Businesses face critical decisions every day that can have significant consequences, and deciding whether to bring someone on as an employee or a contractor ranks among the most important choices business owners make. While classifying workers as independent contractors may seem more manageable—less paperwork, fewer taxes, more flexibility—failure to classify properly can lead to serious legal trouble. The IRS may enforce penalties, interest, or even jail time in some circumstances. This guide is designed to help you avoid that mess and determine who should receive a 1099 and who truly needs a W-2.

Workers classified by the IRS as independent contractors have greater autonomy and control over their work than employees and function like their own bosses. They are typically hired to perform specific tasks or services, but how they complete the work is primarily up to them. They set their own hours, meaning they usually decide when and how long they work, without needing to clock in or out. They also often use their own tools or equipment, such as laptops, trucks, or specialized gear.

Importantly, contractors can work with multiple clients simultaneously since they usually aren't bound exclusively to a single business. For most contractors, there's no benefits package: no health insurance, paid time off, or retirement contributions. They typically submit invoices for payment and receive a 1099-NEC form at tax time, requiring them to manage all their own taxes, including self-employment tax, since no taxes are withheld from their payments.

Individuals the IRS classifies as employees are under the control of the entity they work for. The employer sets the schedule, determines how the work should be completed, and provides the necessary tools or workspace. Typically, employees work primarily for one entity. Employees may receive benefits that are often not provided to independent contractors, including employer-sponsored health insurance, paid time off, retirement savings plans such as 401(k) accounts, and other workplace benefits.

Additionally, employers handle tax obligations by withholding federal income taxes and Social Security and Medicare contributions directly from employee paychecks. At tax time, employees receive Form W-2s, which document their annual earnings and the total amount of taxes withheld and remitted to tax authorities on their behalf.

The IRS makes it crystal clear: no single factor is determinative. The determination requires a comprehensive evaluation of all relevant factors and circumstances. The IRS examines the entire working relationship through three key categories—behavioral control, financial control, and the type of relationship.

Behavioral Control examines whether the business controls what the worker does and how the work is done. Does the business dictate work hours, tools used, or procedures followed? If you, as a business owner, can direct and control when, where, and how a worker performs their job, including the specific techniques they must use and the procedures they must follow, the worker may be an employee. Independent contractors typically have more freedom to determine how they complete their work.

Financial Control looks at who controls the financial aspects of the job. How is the worker paid? Are expenses reimbursed? Is there a risk of financial loss for the worker? Employees are generally paid a regular wage or salary, and the employer may provide the tools and products needed. In contrast, independent contractors usually invest in their own tools, cover their own expenses, and are often paid a flat fee per job or project. They have the opportunity to realize a profit or incur a loss based on their own business decisions.

Type of Relationship considers what the contract says, whether the work is ongoing or for a set term, and whether benefits like health insurance or retirement are included. Key factors include whether there is a written contract, the permanency of the relationship, and whether the work performed is a key aspect of the business's operations. A long-term relationship in which the worker provides essential services and is integral to operations may indicate an employee relationship. If the worker is hired for a specific project with a clear end date and there is no expectation of ongoing work, they may be considered an independent contractor.

The greater the degree of control a business exercises over the methods, timing, and scope of work performed, and the more closely the working relationship mirrors conventional employment arrangements, the stronger the indication that the worker should be classified as a W-2 employee rather than an independent contractor.

The professional team from Azarvand Tax Law.

Azarvand Tax Law

Employers are expected to understand the difference and classify their workers correctly; however, the IRS makes the final determination. An employer or worker can file Form SS-8, Determination of Worker Status for Purposes of Federal Employment Taxes and Income Tax Withholding, which is a tool for both business owners and service providers to determine correct classification. If the balancing factors indicate that a contractor should be classified as an employee, despite their employer issuing a 1099, the worker may still be entitled to the legal rights and tax treatment of a W-2 employee, and the employer can be liable for significant penalties.

Not exactly. While the IRS focuses on how taxes are handled, the Department of Labor examines whether a worker is entitled to protections under laws such as the Fair Labor Standards Act, which covers aspects like minimum wage, overtime, and rest breaks. The DOL uses its own test for determining classification, often applying a stricter "economic realities" standard.

The economic realities test asks a fundamental question: Is the worker economically dependent on the employer, or is the worker truly in business for themselves? This test examines factors such as whether the work is integral to the employer's business, the worker's opportunity for profit or loss based on their own initiative and investment, the permanence of the working relationship, and the nature and degree of control the employer exercises. Under this framework, even workers with significant day-to-day autonomy may still be classified as employees if they are economically dependent on a single business for their livelihood.

A worker might be treated as an independent contractor for tax purposes but still qualify as an employee under labor law. Even if you dodge IRS penalties, the DOL has its own penalties that it enforces. Businesses should be aware that checking one box doesn't mean they are in the clear, which is why reaching out to a tax professional is crucial.

The IRS and DOL take worker classification seriously, and the consequences can be steep, even for honest mistakes. When workers are misclassified, the consequences can be severe and long-lasting, potentially including penalties, accrued interest, increased FICA taxes, and even prison time if done intentionally. It is also important to note that in instances of willfulness, the person responsible for withholding taxes could be held personally liable for any uncollected tax.

Even without any bad intent, penalties can add up quickly. Under Internal Revenue Code Section 3509, if an employer filed proper Forms 1099 for the workers, the reduced penalties include 1.5% of wages for failure to withhold income taxes and 20% of the employee's share of FICA taxes that were not withheld. However, if the employer failed to file required Forms 1099 or W-2, the penalties increase significantly: 3% of wages for failure to withhold income taxes and 40% of the employee's share of FICA taxes. In either scenario, the employer also owes 100% of the employer's matching share of FICA taxes, plus a failure-to-pay penalty of 0.5% of the unpaid tax liability for each month, up to 25% total. Interest also accrues on these penalties from the original due date.

Additionally, the IRS imposes penalties for each missing Form W-2. For returns due after December 31, 2025, these penalties are $60 per Form W-2 if filed within 30 days after the due date (maximum $683,000 per year for most businesses), $130 per form if filed more than 30 days late but by August 1 (maximum $2,049,000 per year), and $340 per form if filed after August 1 or not filed at all (maximum $4,098,500 per year).

If the IRS believes the misclassification was willful or fraudulent, the reduced rates under Section 3509 do not apply at all, and the employer faces full liability for all taxes that should have been withheld and paid. Criminal penalties may include up to one year in prison and fines. The penalties for failing to file required Forms W-2 also increase: for returns due after December 31, 2025, intentional failure to file can result in penalties of up to $660 per form. Additional fines and penalties from the Department of Labor are also possible in cases of intentional misclassification.

The salon and beauty industry presents unique situations that can lead to confusion regarding worker classification. Booth renters, for example, often set their own hours and prices, are responsible for their own supplies and products, and pay fixed rent to the salon owner. In many cases, booth renters are independent contractors. However, if the salon owner controls how the stylist operates—such as dictating work hours, requiring specific products, or setting prices—the stylist may be classified as an employee.

Commission-based stylists present another common scenario. If these stylists must work specific hours, follow salon procedures, and use salon-provided tools and products, they may be employees despite being paid through commissions. The level of control the salon owner exercises is a key determinant of their classification. Freelance stylists who work at multiple salons or take on private clients outside the salon may be brought in for specific events or busy periods. If these stylists work independently, set their schedules, and are not subject to salon policies, they may be independent contractors. However, if a freelance stylist has a long-term, ongoing relationship with one salon where they are expected to work regularly and adhere to salon procedures, they may be considered an employee.

Apprentices and assistants often work closely with more experienced stylists, learning the trade and providing support services. If they work under the direct supervision of salon staff, follow a set schedule, and use salon-provided tools, they are generally classified as employees.

When in doubt, err on the side of caution and seek help from a certified tax professional. Getting it wrong, even as an honest mistake, can be expensive. If you're concerned that you have been

misclassified or that you have misclassified someone else in your business, talk to a qualified tax professional immediately. To avoid the pitfalls of worker misclassification, business owners should review the classification of their workers regularly, assess the degree of control they have over each worker, examine the financial arrangements, and evaluate the nature of the relationship.

Correctly classifying workers as employees or independent contractors is essential for maintaining legal compliance, avoiding financial penalties, and ensuring the smooth operation of your business. With careful attention to the IRS guidelines and a proactive approach to compliance, you can make informed decisions that protect your business and support its growth.

This guide offers a general overview of IRS worker classification rules, but it is not a substitute for legal or tax advice. Regulations change, enforcement priorities shift, and your specific facts matter. If you're unsure about how to classify a worker, or think you've been misclassified yourself, consult with a qualified tax professional.

For personalized advice based on your specific circumstances, contact Azarvand Tax Law at Info@AzarvandTaxLaw.com or book a free consultation at AzarvandTaxLaw.com.

Starting at Impressions front desk in 2006 when he was 19 years old, General Manager Paul Petrowsky is a seasoned professional who owner Sarah Taylor says is responsible for much of her own success.

Planning is in full swing for the most anticipated events and promotions for the 2026 holidays. As owners share their favorite ways to celebrate, they prove that a carefully planned event can also build culture, increase client loyalty, boost sales, and set a business up for a successful 2027.

When things run amok at Mane Attraction Salon, Owners Chris and Jenny Knudsen say General Manager Sami Hernandez is their go-to resource and ultimate sounding board. Meet Sami in this installment of Meet the Manager.

Pagoda, a new AI-native operating system for scheduling, payments, patient records, marketing, and client communications, launches at Skinovatio Medical Spa in Arlington Heights, Illinois.

At a panel discussion hosted by L’Oréal Professionnel in Paris in early July, French Philosopher Sophie Galabru explored the cultural shift where women are increasingly choosing natural, personalized color results over traditional grey coverage. In an exclusive interview with SALON TODAY, Galabru and L’Oréal Professionnel Colorist Pierrick Beringer discuss this shift and how salons and colorists respond.

At Salon Blonde, Director of Operations treats the staff as the salon's most important guests, while her wonderful 'nerdy' side, loves data, systems, and numbers. Find out how she makes Salon Blonde tick.

In an exclusive interview with SALON TODAY, Salon Owner Salvatore Minardi reflects on his past 18 months as Intercoiffure America Canada's World Talent Exchange Ambassador and how his experiences will help encourage cultural and artistic exchange and support greater engagement between ICA and the global organization Intercoiffure Mondial.

Everything you need to know about client retention as a salon owner.

Owner Shelby Bills says her general manager, Sydney Osborne, reminds her of the power of leading with heart. Find out how Osborne became a great leader in our lastest installment of Meet the Manager.

In her latest blog, Kati Whitledge identifies the five stages salon owners go through when a team member leaves the salon unethically, offering advice for each stage.

The beauty and wellness businesses pulling ahead aren’t just working harder—they’re using AI to capture demand, personalize pricing, and convert more of every guest interaction into revenue. Here’s what the benchmark data reveals about the growing gap between AI adopters and everyone else.

Sponsored by Zenoti

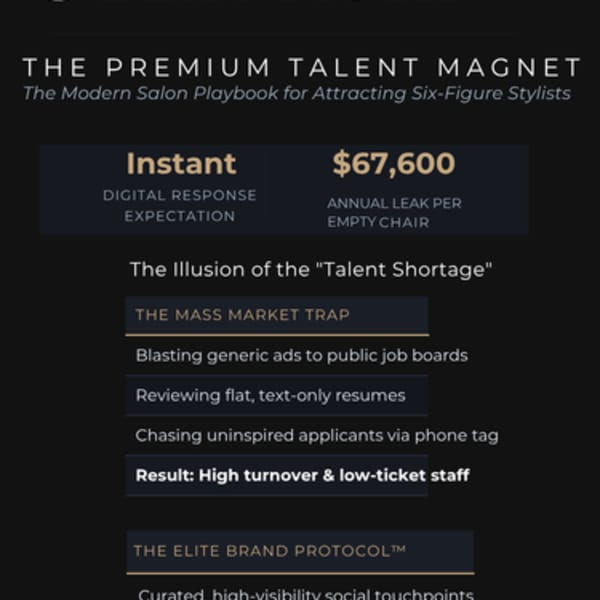

Stop chasing recruitment ghosts on generic job boards and start curating an elite team. Discover the framework that top-tier salons use to bypass phone tag, automate visual portfolio vetting, and attract high-earning, culture-first beauty professionals directly through real-time messaging. Turn your recruitment process into an exclusive brand invitation that keeps your highest-ticket chairs permanently filled.

Sponsored by Beautista

Your calendar looks full, but is all of that demand actually converting to revenue? From phantom rebookings to underpriced peak hours, the 2026 Benchmark Report exposes five revenue leaks that most beauty and wellness businesses don’t even know they have.

Sponsored by Zenoti

After moving to Colorado and teaching at a cosmetology school, Allison Stock joined Zandi K as a stylist, eventually becoming part of the Leadership Team, Education Team and Master Bridal Team. Today, as Director of Operation, Stock is Owner Nicki Wenz's right hand, managing human resources and operations, education and career development, and coaching and culture.

In a world dominated by e-commerce, salon owners push back with proven strategies to increase retail sales while motivating team members to educate their clientele and delighting clients with retail-themed events and clever merchandising displays.

The company's Concealed Bead Method is raising the bar for what professional extension education can deliver.

Scott maximized her micro-salon by transitioning from stylist to strategic owner, focusing on recruiting and station-sharing. By prioritizing her ownership role over behind-the-chair work, she grew her team to six stylists within the two-chair, 150-square-foot space before eventually moving to a larger facility.